Introduction

Missing three consecutive Form 990 filings automatically revokes your nonprofit's tax-exempt status. According to the IRS, organizations lose the ability to receive tax-deductible contributions and may suddenly owe corporate income tax—a scenario that has caught hundreds of nonprofits off guard.

IRS Form 990 is the annual information return that tax-exempt organizations must file to maintain exempt status. While nonprofits are generally exempt from federal income tax, the IRS requires Form 990 as a mandatory accountability report. This filing exposes your organization's finances, governance practices, and compensation structures to public scrutiny.

Many nonprofit leaders struggle with Form 990 deadlines, variant selection (990-N, 990-EZ, or full 990), and disclosure requirements. Without dedicated finance staff, understanding what's required, when it's due, and how to avoid penalties becomes critical to protecting your organization's mission and financial health.

TL;DR

- Form 990 ensures tax-exempt nonprofits operate legitimately and manage funds responsibly

- Most tax-exempt organizations must file annually; the version depends on size and type

- Filing deadline is 5 months after fiscal year-end; 6-month extensions available via Form 8868

- Form 990 is a public document—donors, funders, and watchdog organizations regularly review it, making accuracy and transparency critical

- Failing to file for three consecutive years results in automatic revocation of tax-exempt status

What Is IRS Form 990 and Who Must File?

Form 990 is officially titled "Return of Organization Exempt From Income Tax." It functions as an annual accountability report—not a tax payment document—designed to demonstrate that your organization continues to merit its exempt status.

Organizations Required to File

Most tax-exempt organizations recognized by the IRS under section 501(a) must file Form 990 annually, including:

- 501(c)(3) organizations (charitable nonprofits)

- Other 501(c) tax-exempt associations (social welfare, labor, business leagues)

- Private and public foundations

- Independent educational institutions

- Private healthcare organizations

Organizations Exempt from Filing

The following categories are exempt from the Form 990 requirement:

- Churches, interchurch organizations, and conventions or associations of churches

- Integrated auxiliaries of a church

- Exclusively religious activities of any religious order

- Corporations organized under an Act of Congress that are instrumentalities of the United States

- State institutions whose income is excluded under IRC Section 115

- Governmental units or affiliates meeting specific IRS requirements

Critical distinction: Being tax-exempt does not mean being filing-exempt. Most tax-exempt organizations must file Form 990 even though they don't owe federal income tax.

Beyond federal requirements, most states also require charitable nonprofits to file separate state-level registrations, and many states accept the federal Form 990 for required financial disclosures.

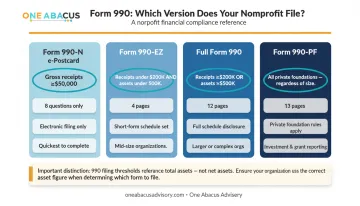

Which Version of Form 990 Does Your Nonprofit File?

The correct version is determined by your organization's annual gross receipts and total assets. Here's the breakdown:

Form 990-N (e-Postcard)

This minimal 8-question electronic notice applies to organizations with annual gross receipts of $50,000 or less. Key details:

- Cannot be paper-filed (electronic only)

- No late filing penalty

- Failing to file for three consecutive years still triggers revocation

- Requires eight items: EIN, tax year, legal name, mailing address, other names used, principal officer contact, website address, and confirmation of gross receipts

Form 990-EZ

This shortened 4-page version applies to organizations with:

- Gross receipts under $200,000, AND

- Total assets under $500,000

- Both conditions must be met

- Electronic filing required for tax years ending July 31, 2021 and later

Full Form 990

This comprehensive 12-page return is required when gross receipts total $200,000 or more OR total assets equal $500,000 or more.

Key filing considerations:

- Only one threshold needs to be met (not both)

- Uses total assets from balance sheet, not net assets

- Organizations often miscalculate by reporting net assets instead

- This is the most commonly missed distinction when determining form type

Form 990-PF

All private foundations must file this 13-page form regardless of size. Required disclosures include:

- Private assets and trustee information

- Detailed grant awards and recipients

- Revenue and expense analysis

- Balance sheets and officer compensation

- More extensive disclosures than standard Form 990

Form 990 Filing Deadlines, Extensions, and the Filing Process

Core Deadline Rule

Form 990 is due on the 15th day of the 5th month after the end of your organization's fiscal year.

Common examples:

- Calendar-year filers (Jan-Dec): May 15

- July-June fiscal year: November 15

Extension Option

Nonprofits can request an automatic 6-month extension by filing Form 8868 by the original due date. Important notes:

- The 990-N deadline cannot be extended

- No penalty applies for late 990-N submission

- Extensions don't eliminate the filing requirement

Mandatory E-Filing Rule

Under the Taxpayer First Act of 2019, all Form 990s, 990-EZs, 990-PFs, and 990-Ts for tax years beginning after July 1, 2019 must be filed electronically through an IRS-authorized e-file provider. Paper filing is no longer an option for current-year returns.

What Goes Into the Filing

Understanding what the IRS requires helps you prepare efficiently. The form requests detailed information across several categories:

- Program descriptions: Detailed narratives of your three largest programs

- Financial statements: Revenue, expenses, net assets

- Governance policies: Conflict of interest, whistleblower, document retention

- Compensation: Officers and key employees

- Schedules: For larger organizations, details on fundraising, grants, and related transactions

Professional Support

Many nonprofits—particularly those without dedicated finance staff—work with a nonprofit-specialized accounting advisor or fractional CFO to ensure accurate, timely filing.

This support often includes financial statement preparation, governance documentation, and schedule completion. For organizations managing complex grants or multiple revenue streams, fractional CFO services provide the expertise needed to complete Form 990 correctly while strengthening year-round financial oversight.

Penalties and Consequences of Not Filing Form 990

Late Filing Penalty Structure

According to the IRS late filing procedures:

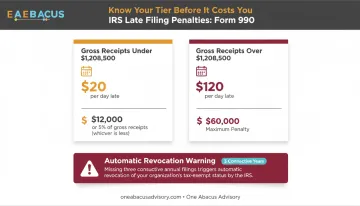

Organizations with gross receipts under $1,208,500:

- $20 per day late

- Maximum penalty: $12,000 or 5% of gross receipts, whichever is less

Organizations with gross receipts exceeding $1,208,500:

- $120 per day late

- Maximum penalty: $60,000

Automatic Revocation—The Most Serious Consequence

If your nonprofit fails to file Form 990 for three consecutive years, the IRS automatically revokes your tax-exempt status under IRC Section 6033(j).

The consequences are severe:

- The organization loses its ability to receive tax-deductible contributions

- The organization may owe corporate income tax

- Requires filing a new Form 1023 application and paying additional fees to regain status

While these penalties are significant, relief options exist for organizations facing filing challenges.

Reasonable Cause Exceptions

You can request penalty relief by demonstrating reasonable cause for late filing. The IRS considers:

- Written explanation of all extenuating circumstances

- Documentation supporting your claim

- Evidence of good faith effort to comply

Filing an extension is the most reliable way to avoid penalties if you anticipate missing the deadline—request Form 8868 before your original due date.

Why Form 990 Matters More Than Just Compliance

Public Document Status

Under IRC 6104(d), Form 990 is a public document. Organizations must provide copies of their three most recent returns to anyone who requests them.

The public can find your Form 990 on:

- IRS Tax Exempt Organization Search (TEOS)

- ProPublica's Nonprofit Explorer

- Candid (formerly GuideStar)

Donors, funders, grant reviewers, and watchdog organizations regularly review these filings before making funding decisions.

Governance and Transparency Signal

Because Form 990 is publicly visible, it becomes a governance signal. Part VI asks about:

- Board policies (conflict of interest, whistleblower, document retention)

- Executive compensation processes

- Related-party transactions

- Program effectiveness

A well-prepared 990 signals organizational integrity and actively supports donor confidence and grant eligibility.

Organizations that treat Form 990 as a strategic communication tool (by proactively posting filings and documenting governance policies) strengthen trust with funders and stakeholders.

Strategic Planning Connection

The financial data disclosed on Form 990 provides valuable insights:

- Revenue trends

- Expense ratios

- Net asset balances

This gives nonprofit leaders and boards a structured annual look at organizational health.

A fractional CFO can help interpret this data to drive better decisions year-round, turning a compliance exercise into a planning tool. For example, fractional CFO services at One Abacus Advisory provide executive-level oversight that translates Form 990 insights into actionable budgeting, forecasting, and board-ready analysis.

Common Form 990 Mistakes and Misconceptions

Most Common Misconceptions

"Tax-exempt status means no filing is required"

- Not true. Most tax-exempt organizations must file annually, with limited exceptions for churches and government entities.

"The 990 only matters to the IRS"

- Far from it. Donors, funders, and watchdog organizations actively use Form 990 to evaluate nonprofits before making funding decisions.

"Organizations can still file on paper"

- No longer an option for most. Current e-file mandates apply to tax years beginning after July 1, 2019.

"Small nonprofits are off the hook entirely"

- Not quite. Organizations with gross receipts under $50,000 still need to file Form 990-N.

Beyond these misconceptions, preparatory errors create real compliance risks.

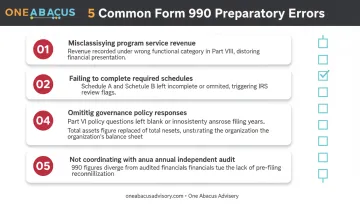

Most Frequent Preparatory Errors

- Misclassifying program service revenue: Revenue categories must be reported correctly in Part VIII

- Failing to complete required schedules: Missing schedules like Schedule A (public charity status) or Schedule B (contributor information) creates an incomplete return

- Omitting governance policy responses: Part VI governance questions signal organizational integrity to donors and funders

- Reporting net assets instead of total assets: This causes organizations to file the wrong form version

- Not coordinating with an annual independent audit: Audit prep should be completed before Form 990 submission to ensure consistency

One Abacus Advisory works with nonprofits to address these gaps during audit preparation—reviewing financial records, strengthening reconciliations, and improving documentation before fieldwork begins.

Frequently Asked Questions

Do nonprofits have to file Form 990?

Yes. Most tax-exempt organizations recognized by the IRS under section 501(a) must file annually, with limited exceptions for churches and government entities. Failing to file carries penalties and risks revocation of exempt status.

Are Form 990 tax filings public?

Yes. Form 990s are public records. Organizations must make their three most recent returns available upon request, and filings are searchable through IRS TEOS, ProPublica, and Candid.

Where can I find Form 990 filings for nonprofits online?

The main sources are the IRS Tax Exempt Organization Search (TEOS), ProPublica's Nonprofit Explorer, and Candid (formerly GuideStar), which collectively host millions of returns going back to the early 2000s.

What happens if a nonprofit fails to file Form 990?

Penalties range from $20 to $120 per day with caps between $12,000 and $60,000. The critical risk is automatic revocation of tax-exempt status after three consecutive years of non-filing.

What is the difference between Form 990, 990-EZ, and 990-N?

Form 990-N is for organizations under $50,000 in receipts, 990-EZ for those under $200,000 in receipts and $500,000 in assets, and full Form 990 for larger organizations. Private foundations always file 990-PF regardless of size.

Can a nonprofit request an extension to file Form 990?

Yes. File Form 8868 by the original due date for an automatic 6-month extension. The 990-N cannot be extended but has no late penalty. Extensions delay the deadline but don't eliminate the filing requirement.

Need help with Form 990 preparation or nonprofit financial leadership? One Abacus Advisory provides fractional CFO services, audit preparation, compliance oversight, and comprehensive accounting support tailored to nonprofit organizations. Contact Lorin Port at lorin@oneabacusadvisory.com or call 760-845-3808 to discuss how flexible, right-sized financial leadership can strengthen your organization's compliance, governance, and strategic decision-making.