Introduction

Financial statements often feel like documents prepared for auditors, not for the leaders who need them most. Dense columns of numbers and unfamiliar terminology obscure the strategic insights these reports contain.

Yet when understood properly, your organization's four core financial statements become powerful leadership tools, not just compliance paperwork.

This guide reframes the Statement of Activities, Statement of Financial Position, Statement of Cash Flows, and Statement of Functional Expenses as decision-making instruments. They answer the questions every nonprofit leader and board needs answered: Are we financially healthy? Are we using resources wisely? Can we sustain our mission?

Together, these four statements tell your organization's complete financial story—revealing not just where you stand today, but whether you're positioned to deliver on your mission tomorrow.

TLDR

- Each statement reveals different financial health: surplus/deficit performance, asset/liability position, actual cash flow, and mission spending allocation

- Track "net assets" (not equity) and separate donor-restricted from unrestricted funds to maintain compliance

- 52% of nonprofits have three months or less of cash reserves, making cash flow monitoring critical

- Review all four statements together monthly or quarterly to spot patterns no single report reveals

- Build funder confidence and strengthen fundraising through accurate, transparent financial reporting

Why Nonprofit Financial Statements Matter Beyond Compliance

GAAP-compliant financial statements are required for audits, Form 990 filings, and many grant applications. But their real value lies in the decisions they enable—from budgeting and program expansion to board oversight and strategic planning.

Serving Multiple Stakeholders

Financial statements serve different audiences with distinct needs:

- Boards use them to fulfill fiduciary duty and monitor organizational health

- Grantmakers assess stability before awarding funding—many foundations require audited financials as part of due diligence

- Donors verify responsible stewardship before making major gifts

- Leadership teams track performance against budget and identify emerging issues

These diverse needs have shaped how nonprofit financial reporting has evolved. FASB ASU 2016-14, effective for fiscal years beginning after December 15, 2017, was the first significant revision to nonprofit financial reporting since 1993. This update simplified net asset classifications and expanded functional expense reporting requirements, making statements more useful for decision-making.

How Nonprofits Differ from For-Profits

These reporting standards reflect a fundamental difference in organizational purpose. Nonprofit financial statements emphasize stewardship of contributed resources rather than profit generation:

- Net assets replace equity on the balance sheet

- Donor restrictions must be tracked separately (with vs. without donor restrictions)

- Functional expenses show mission spending vs. administrative costs

- Terminology emphasizes accountability to donors and the public

Producing accurate, readable statements builds trust that directly supports fundraising and mission delivery.

When your financials clearly demonstrate fiscal discipline, funders respond with confidence.

Statement of Activities: Tracking Revenue, Expenses, and Net Assets

The Statement of Activities is the nonprofit equivalent of an income statement. It covers a specific period—typically the fiscal year—and shows whether your organization operated at a surplus or deficit.

The statement compares total revenues against total expenses to reveal your financial position.

What's Included

The statement contains three core sections:

1. Revenue and Support

- Individual donations

- Foundation and corporate grants

- Government contracts

- Program service fees

- Investment returns

- In-kind contributions

According to Giving USA 2025, U.S. charitable giving reached $592.50 billion in 2024, with individuals contributing approximately 67% ($392.45 billion) of total giving.

This dominance of individual giving underscores why donor retention and acquisition strategies matter so much to your bottom line.

2. Expenses

- Organized by function: program services, management and general, fundraising

- Detailed breakdown appears in the Statement of Functional Expenses

3. Change in Net Assets

- The bottom-line result showing whether net assets grew or shrank

- Presented in two columns: with donor restrictions and without donor restrictions

The Critical Distinction: Restricted vs. Unrestricted Net Assets

Net assets with donor restrictions are funds earmarked for specific purposes or time periods by the donor. Net assets without donor restrictions are available for any mission-aligned use.

When restricted funds are spent as intended, you must record a release from restriction—simultaneously decreasing restricted net assets and increasing unrestricted net assets. This reclassification appears on the Statement of Activities and reflects that donor conditions have been satisfied.

What Leadership Should Watch For

Use this statement actively throughout the year—not just at year-end. Compare actual revenue and expenses against your operating budget monthly or quarterly.

Significant variances signal issues requiring corrective action:

- Large shortfall in individual giving vs. budget suggests donor retention problems

- Program expenses running 20% over budget indicate cost control issues

- Delayed grant revenue may require cash flow adjustments

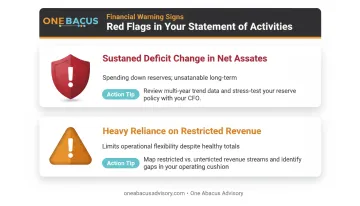

Two critical red flags:

- Sustained deficit change in net assets - Your organization is spending down reserves, which cannot continue indefinitely

- Heavy reliance on restricted revenue with limited unrestricted funds - Even when overall numbers look healthy, operational flexibility suffers when most resources carry restrictions

Statement of Financial Position: Your Organization's Financial Snapshot

The Statement of Financial Position (also called the balance sheet) is a point-in-time snapshot—typically at fiscal year-end—showing what your organization owns, what it owes, and what remains as net assets.

The fundamental equation: Assets = Liabilities + Net Assets

What's Included

Assets (listed by liquidity):

- Current assets: Cash, accounts receivable, pledges receivable, prepaid expenses

- Noncurrent assets: Property, equipment, investments, endowments

Liabilities (listed by due date):

- Current liabilities: Accounts payable, accrued expenses, deferred revenue, current portion of debt

- Noncurrent liabilities: Mortgages, long-term notes, pension obligations

Net Assets (broken into two categories):

- With donor restrictions

- Without donor restrictions

Positive net assets indicate financial health. Negative net assets require immediate board attention and corrective action.

Nonprofit-Specific Line Items That Cause Confusion

Understanding the equation is one thing. Interpreting nonprofit-specific terminology is another.

Pledges Receivable

These are promises to donate not yet received. Under GAAP, unconditional pledges are recognized as revenue and as a receivable when the promise is made—not when cash arrives. Multi-year pledges are recorded at present value.

This distinction matters: $100,000 in pledges receivable is not the same as $100,000 in cash. Your bank account may be empty even when your balance sheet shows significant receivables.

Deferred Revenue

Funds you've received but not yet earned—typically from exchange transactions like tuition, event registrations, or membership fees. It appears as a liability until you deliver the promised service, at which point it becomes revenue.

Board-Designated Net Assets

Unrestricted funds the board has voluntarily set aside for specific purposes (sometimes called "quasi-endowments"). These remain classified as "without donor restrictions" because the board—not a donor—imposed the restriction and can reverse it at any time.

What Leadership Should Watch For

Positive net assets does not mean you have cash available. Liquidity—your ability to cover short-term obligations—is what matters day-to-day.

Examine the ratio of current assets to current liabilities:

- Current assets: $50,000 (mostly cash)

- Current liabilities: $45,000 (due next month)

- Result: Tight liquidity despite technical solvency

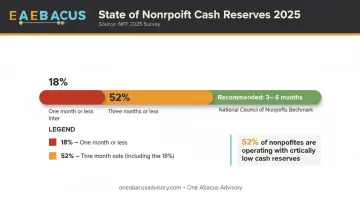

The National Council of Nonprofits recommends three to six months' worth of operating costs as an operating reserve goal.

Yet NFF's 2025 survey found that 52% of nonprofits have three months or less of cash on hand, and 18% have one month or less.

This matters beyond internal planning. Grantmakers and lenders frequently request this statement to assess stability before awarding significant funding. Adequate unrestricted net assets signal financial resilience and management competence.

Statement of Cash Flows: Where the Cash Actually Goes

The Statement of Cash Flows tracks actual cash moving in and out—distinct from the Statement of Activities, which uses accrual accounting.

Here's the essential point: Your organization can show positive net assets on accrual financials while still running out of cash. This happens when the timing of receipts and payments doesn't match. Net assets support the mission long-term; cash pays the bills today.

What's Included

Operating Activities cover day-to-day cash movements:

- Cash inflows: donations received, grants paid out, program fees collected

- Cash outflows: payroll, rent, program costs

Investing Activities include:

- Purchases of long-term assets (equipment, investments)

- Proceeds from selling long-term assets

Financing Activities:

- Borrowing and repaying debt

- Contributions restricted for long-term purposes (endowments, capital campaigns)

The net change across all three categories explains why cash increased or decreased during the period.

Why This Statement Matters Most for Operations

Monitor this statement monthly or quarterly, not just annually. Seasonal giving patterns, delayed grant reimbursements, and payroll timing create cash crunches even in financially healthy organizations.

NFF's 2025 survey revealed that 38% of nonprofits experienced delays in government funding that impacted cash flow, and 36% ended 2024 with an operating deficit. Early visibility prevents overdrafts and missed payroll.

A practical example: You may recognize $100,000 in multi-year pledges on your Statement of Activities (increasing net assets). But if only $25,000 arrives in cash this year, your Statement of Cash Flows shows the reality your bank account experiences.

Statement of Functional Expenses: Showing Mission in Action

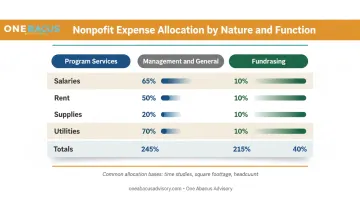

The Statement of Functional Expenses is unique to nonprofits. It presents a matrix showing expenses classified both by nature (what was purchased: salaries, rent, supplies) and by function (why it was purchased: program delivery, management, fundraising).

FASB ASU 2016-14 now requires all nonprofits presenting audited statements to show this dual classification. Previously, only voluntary health and welfare organizations faced this requirement.

What's Included and How Allocation Works

Three functional columns:

- Program Expenses - Directly advancing the mission

- Management and General - Operations and administration

- Fundraising - Generating contributed revenue

Some expenses fit cleanly into one column (a grant writer's salary = 100% fundraising). Others must be allocated across multiple functions (an executive director's time split across program oversight, management, and fundraising).

Allocations must be:

- Documented with clear methodology

- Consistently applied year over year

- Defensible to auditors and grantmakers

Common allocation bases include time studies, square footage, headcount, or direct usage tracking.

These allocation requirements matter because stakeholders scrutinize how nonprofits divide resources between mission work and overhead.

The Overhead Ratio Question

The BBB Wise Giving Alliance sets a benchmark that charities should spend at least 65% of total expenses on program activities. This remains the most widely cited minimum.

The ideal ratio varies significantly by organizational context:

- Organization age and stage of growth - Startups need infrastructure investment

- Mission type and service delivery model - Direct service differs from advocacy

- Geographic scope and complexity - Multi-state operations require more infrastructure

- Size and infrastructure needs - Smaller budgets mean higher overhead percentages

In 2013, the CEOs of GuideStar, Charity Navigator, and BBB Wise Giving Alliance launched the "Overhead Myth" campaign, cautioning against using overhead ratios as the sole measure of effectiveness.

Their message: focusing exclusively on overhead starves nonprofits of investments in training, planning, evaluation, and internal systems. This creates what the Stanford Social Innovation Review termed the "nonprofit starvation cycle."

The bottom line: Transparency about overhead is more valuable than hitting an arbitrary percentage. Don't make cuts that undermine effectiveness just to improve optics.

How the 4 Statements Work Together to Tell Your Financial Story

No single statement gives the complete picture. Each provides a different lens, and reviewing them together reveals insights invisible in isolation.

How They Interconnect

- The Statement of Activities shows whether net assets changed during the year

- The Statement of Financial Position shows what those net assets look like on the ground

- The Statement of Cash Flows explains why cash moved differently than net assets suggest

- The Statement of Functional Expenses shows how spending was deployed across mission and operations

A Practical Scenario

Consider an organization that reports:

- Statement of Activities: $50,000 surplus (looks healthy)

- Statement of Financial Position: Most assets are property and equipment, minimal cash (liquidity concern)

- Statement of Cash Flows: Negative operating cash flow of $30,000 (immediate problem)

- Statement of Functional Expenses: Administrative costs rising faster than program spending (efficiency question)

Combined, these reveal a very different story than the surplus alone suggests.

The organization may be asset-rich but cash-poor, with operational efficiency declining despite positive net asset growth.

Strategic Decision-Making

When reviewed as a set rather than in isolation, these statements enable:

- Assessing readiness to launch new programs

- Preparing for audits with complete documentation

- Making compelling cases to major funders

- Identifying emerging financial risks early

Nonprofit boards benefit from having a financial leader who can translate these four statements into clear, actionable insights. Many organizations find that fractional CFO services from firms like One Abacus Advisory provide this senior-level financial guidance without the cost of a full-time hire.

Recommended Review Frequency

Annual preparation is the minimum for:

- Audits

- Form 990 filing

- Grant reporting

Monthly or quarterly review is best practice for:

- Board oversight

- Management decisions

- Proactive financial management

Develop a written financial reporting policy specifying:

- Who prepares each statement

- Who reviews it before board presentation

- How often statements are distributed

- What variance thresholds trigger discussion

This policy creates accountability and ensures consistent board communication throughout the year.

Frequently Asked Questions

What are the four basic financial statements for a nonprofit?

The four core statements are: Statement of Activities (revenue, expenses, and net asset changes), Statement of Financial Position (assets, liabilities, and net assets), Statement of Cash Flows (actual cash movement), and Statement of Functional Expenses (spending by nature and function).

Does a 501(c)(3) have to provide financial statements?

Nonprofits with gross receipts above $50,000 must file Form 990, which requires financial data. Many states, grantors, and lenders also require audited statements, and organizations with federal awards exceeding $1,000,000 must undergo a Single Audit.

Where can I find financial statements for nonprofit organizations?

Form 990 filings are publicly available through the IRS Tax Exempt Organization Search and platforms like Candid/GuideStar. Many nonprofits also publish audited financial statements or financial summaries in their annual reports on their websites.

How do nonprofit financial statements differ from for-profit financial statements?

Nonprofits use "net assets" instead of equity, track donor-restricted vs. unrestricted funds separately, report functional expenses (program, management, fundraising), and use terminology reflecting stewardship of mission-driven resources rather than profit generation for shareholders.

How often should nonprofits prepare financial statements?

Annual preparation is required for audits and Form 990 filing. Best practice is monthly or quarterly review of the Statement of Cash Flows and Statement of Activities for board oversight and proactive financial management.

What is the most important nonprofit financial statement?

Leadership and boards most frequently rely on the Statement of Activities to track performance and the Statement of Financial Position to assess overall financial health. The Statement of Cash Flows is critical for day-to-day liquidity management.